Adrian Vanzyl: Are Rising Interest Rates Impacting House Prices?

The relationship between interest rates and housing markets continues to attract attention across Australia, as analysts, policymakers, and investors assess how changing financial conditions may influence property values.

Business strategist Adrian Vanzyl recently addressed the topic, noting that while many view interest rate movements as a key driver of housing trends, multiple interacting factors shape the broader picture.

“Interest rates are an important component of the housing market, but they operate within a wider system that includes supply, demand, and economic sentiment,” Vanzyl said in a recent commentary.

Borrowing Capacity and Market Dynamics

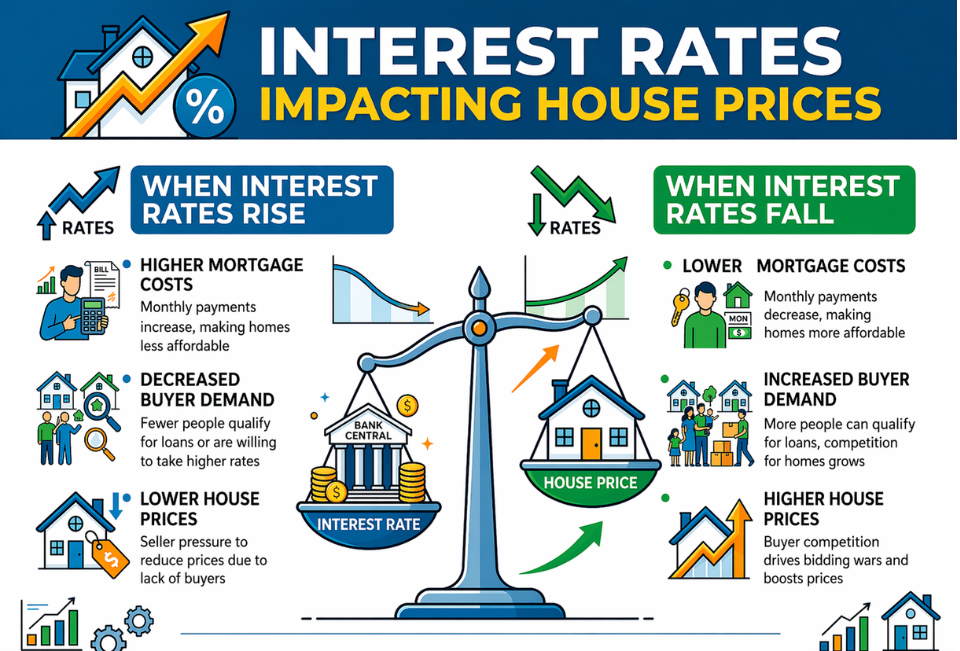

Interest rates are closely linked to borrowing capacity, which can influence how much buyers are able or willing to spend on property. When borrowing costs rise, mortgage repayments may increase, potentially affecting affordability for households.

Economic research suggests that higher interest rates can reduce borrowing capacity and place pressure on demand, while lower rates may have the opposite effect by making financing more accessible.

At the same time, recent data shows that lower interest rate periods have driven rising property values in certain markets, partly due to increased borrowing ability and stronger buyer activity.

However, these relationships are not always uniform across regions or time periods.

A Complex Relationship

Studies examining Australian housing markets indicate that the relationship between interest rates and house prices can vary significantly depending on location and market conditions. In some major cities, price movements have shown a clearer response to rate changes, while in others the connection appears less pronounced.

Analysts often emphasize that interest rates represent just one of several influences. Factors such as population growth, housing supply, income levels, and investor activity also play important roles in shaping market outcomes.

Adrian Vanzyl highlighted this complexity, suggesting that focusing on a single variable may not fully capture the dynamics at play.

“Housing markets are influenced by a combination of economic forces, and isolating one factor rarely provides a complete explanation,” he said.

Supply Constraints and Demand Pressures

In recent months, attention has also been directed toward supply conditions within Australia’s housing market. Reports indicate that limited housing availability and low vacancy rates continue to influence pricing dynamics in both rental and property markets.

At the same time, demand remains present in many areas, supported by population trends and ongoing interest from both owner-occupiers and investors.

Some observers suggest that when supply remains constrained, property prices may show resilience even in the face of higher borrowing costs. Others point to the possibility that reduced affordability could moderate demand over time.

Recent market observations have also noted that buyers may become more cautious during periods of uncertainty, adjusting their expectations and decision-making processes.

Affordability and Consumer Behavior

Affordability remains a central theme in discussions around housing and interest rates. As borrowing costs change, households may reassess their financial position, influencing purchasing decisions and market activity.

Higher mortgage repayments can affect household budgets, potentially leading to shifts in spending priorities. In some cases, this may result in reduced demand for higher-priced properties or increased interest in more affordable segments of the market.

Adrian Vanzyl noted that these behavioral shifts can influence how markets respond over time.

“Changes in affordability can shape buyer behavior, but the outcomes depend on how households adapt to evolving financial conditions,” he explained.

Market Sentiment and Expectations

Market sentiment also plays a role in how interest rate changes are interpreted. Expectations about future rate movements, economic stability, and policy decisions can influence both buyer and seller behavior.

During periods of uncertainty, participants may adopt a more cautious approach, which can affect transaction volumes and pricing trends. Conversely, periods of stability or optimism may support stronger activity.

Analysts often point out that housing markets tend to adjust gradually, rather than responding immediately to single changes in monetary policy.

Broader Economic Context

The broader economic environment remains an important consideration when assessing housing trends. Central banks typically adjust interest rates in response to inflation, employment conditions, and overall economic performance, intertwining their effects with wider economic developments.

This interconnected nature makes it difficult to isolate the impact of any single factor. Instead, housing outcomes are shaped by a combination of financial conditions, market fundamentals, and external influences. Vanzyl emphasized the importance of taking a balanced perspective.

“Understanding housing markets requires looking at how different variables interact over time, rather than relying on one indicator alone,” he said.

Looking Ahead

As Australia’s economic landscape continues to evolve, the relationship between interest rates and house prices is likely to remain a subject of ongoing analysis. While some trends may suggest connections between borrowing costs and property values, the overall picture remains complex and subject to change.

Observers will continue to monitor a range of indicators, including supply levels, demand patterns, and economic conditions, to better understand how the market may develop.

Conclusion

The question of whether rising interest rates are impacting house prices does not have a straightforward answer. While borrowing costs influence affordability and demand, a broader set of factors shapes housing markets, interacting in different ways over time.

As highlighted by Adrian Vanzyl, a comprehensive view of these dynamics may provide a clearer understanding of how economic conditions influence property markets, particularly in an environment marked by both domestic and global uncertainties.